Share Based Remuneration

The net value of Share Based Remuneration (i.e. the gain or benefit arising to an employee on the acquisition of the shares) is to be treated as notional pay for the purposes of calculating employee PRSI only. Employer PRSI is not chargeable on gains from Share Based Remuneration.

The net value means the difference between the market value of the shares awarded and the amount paid by the employee for the shares, where this results in a discount price on the shares, it is this 'discount' which is deemed to give rise to a benefit to the employee.

Any gains arising from the disposal of the shares (proceeds less cost) is within the scope of Capital Gains Tax and is not relevant in the context of Share Based Remuneration. Revenue have issued a specific Tax Manual in relation to Share Based Remuneration.

MEANING OF SHARE BASED REMUNERATION

Share Based Remuneration has a specific meaning for PRSI purposes and is defined in section 2(1) of the Social Welfare Consolidation Act (as amended by Section 10 of the Social Welfare and Pensions Act 2012 and Section 4 of the Social Welfare and Pensions Act 2014). It essentially means remuneration given to an employee in the form of shares (including stock and securities) in the company in which the employee holds his or her office or employment, or in a company which has control of that company.

Shares in any other company do not come within the definition of Share Based Remuneration. All types of share option gains come within the definition.

SHARE AWARDS - THE CHARGE TO PRSI

Remuneration in the form of shares in companies other than that in which the employee holds his or her office or employment, or in a company which has control of that company, has been within the PAYE system since 2004 and remains fully chargeable to both employee and employer PRSI.

Remuneration in the form of shares in the company in which the employee holds his or her office or employment, or in a company which has control of that company, all such share-based remuneration is chargeable to employee PRSI. Employer PRSI is not chargeable.

AMOUNT CHARGEABLE TO PRSI

The receipt of shares by an employee is treated as a perquisite for income tax purposes and the rules that apply to the taxation of notional pay also apply for Employee PRSI purposes. Refer to Revenue guide to Benefit in Kind for further information on the related taxation rules and to what it applies.

RECORDING OF PRSI

As Share Based Remuneration is derived from insurable employment, it should be recorded under the PRSI Class applying to the employee at the time he or she receives the shares (if subject to vesting, the time of vesting) or exercises the share options, as the case may be, even if any benefit or gain accrues to the individual after he or she has left the particular employment.

Because the amount that is chargeable to PRSI is different for employees and employers it may attract different PRSI subclasses.

Where this occurs the return must always be made at the employee's subclass.

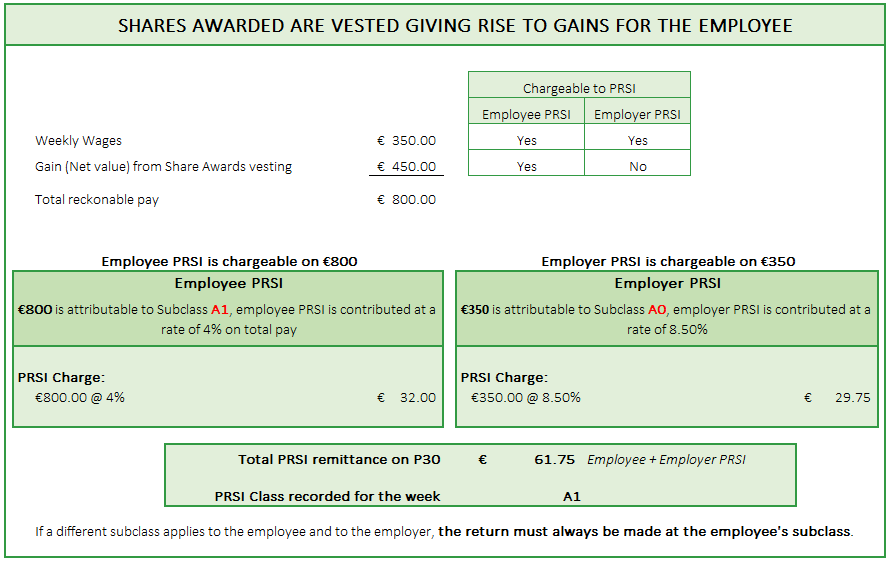

Example:

If a Class A employee has weekly pay of €350 and, in a particular week, has a derived benefit from the issue of shares of €450.

Employee PRSI is calculated on income of €800 - Subclass A1.

Employer PRSI is calculated on income of €350 - Subclass AO.

Employer and employee PRSI should be added together as normal.

Share Based Remuneration: Varying PRSI Subclasses between the employee and employer

PAYMENT OF PRSI

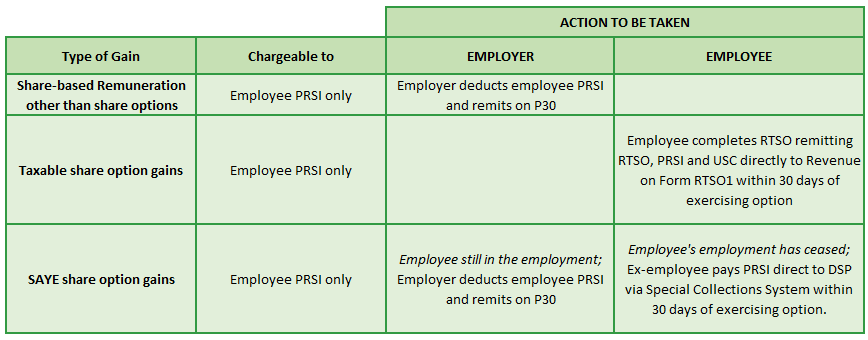

The obligation to deduct and remit PRSI in respect of Share Based Remuneration generally rests with the employer. Accordingly the PRSI payable should be deducted by the employer through payroll along with other PRSI liabilities and remitted to the Collector General with the monthly P30 return.

SHARE OPTION - GAINS

Shares purchased through a Share Option scheme are purchased from an employee's net take home pay. The benefit that the employee may get from exercising a share option is that the option price for buying the shares is less that the market value of the share. The difference between the option price and the market value represents a gain for the employee.

The taxation of gains on the exercise of share options comes within the special self-assessment regime. Income tax known as ‘relevant tax on share options’ (RTSO) is payable within 30 days of an option being exercised and is outside the PAYE collection system. Form RTSO1 must be completed and returned to the Collector General within 30 days of the date of exercise. USC and PRSI on such gains must also be included on the Form RTSO1and remitted, together with the income tax due, within 30 days of exercise.

Refer to the Revenue issued Form CG16 for further information.

SAVE AS YOU EARN SCHEMES (SAYE)

Gains made on the exercise of share options received under Revenue approved SAYE schemes are not chargeable to income tax. In the case of share options exercised when the individual is still employed by the company that granted the share option, the obligation to deduct and remit PRSI rests with that employer. Accordingly, the PRSI should be deducted by the employer through payroll along with other PRSI liabilities and remitted to the Collector General with the monthly P30.

Where a share option is exercised after the individual has left the employment, the obligation to pay the PRSI falls instead on that individual. PRSI should be paid directly to the Department of Social Protection's Special Collection Section within 30 days after the share option has been exercised. Form SBR1 is to be used for this purpose.

PAYMENT ARRANGEMENTS

Share Based Remuneration: Payment Arrangements

PROCESSING SHARE BASED REMUNERATION IN COLLSOFT

Once an employee and employer enter into a shares agreement, the employer must establish which if the categories the share falls into; Share Based Remuneration or a Share option. Once confirmed the employer will identify if it falls into the PAYE collection system and their obligations to deduct and remit the necessary PAYE, USC and PRSI derived from the resulting gains on exercise/vesting.

Recording share gains in CollSoft in order to make the necessary deduction the gains whould be treated as a Benefit in Kind.

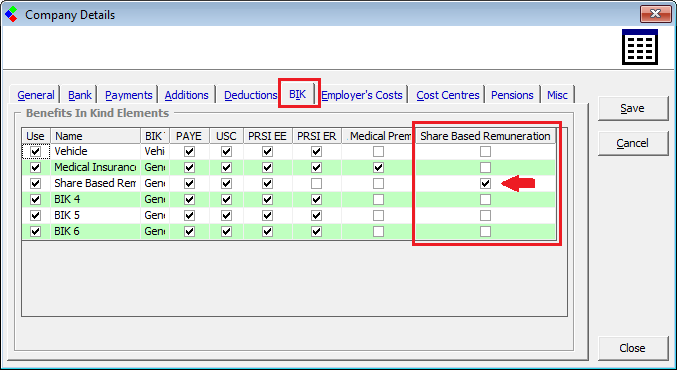

To apply the correct treatment of PAYE, USC, and EmployEE PRSI (but not EmployER PRSI) CollSoft offers a specific Share Based Remuneration flag within Benefit settings.

The first step is to assign a Benefit in Kind setting to 'Share Based Remuneration' at Company level.

ASSIGN A BIK ELEMENT TO TREAT SHARE BASED REMUNERATION

Share Based Remuneration: Assign a BIK element at Company level

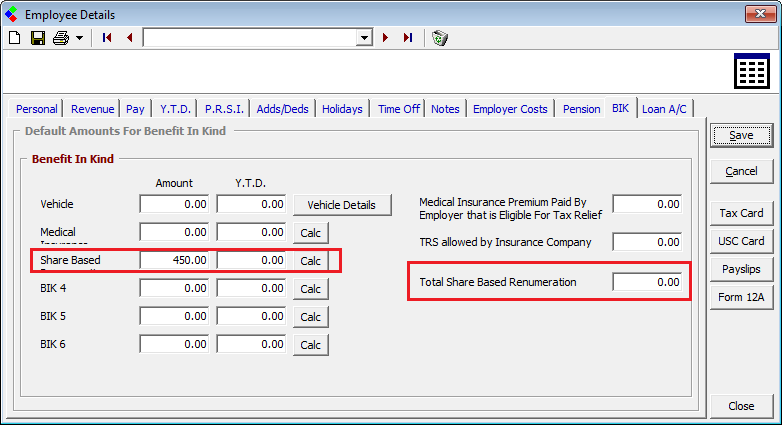

UPDATE THE EMPLOYEE RECORD WITH THE PERIODICAL VALUE

Now that there is a dedicated BIK element, the notional value of the associated share remuneration should be captured within the employees periodical payroll to which it relates (the approriate date to make the deductions should be decided on based on the circumstance in compliance with the Revenue rules for remittance).

Share Based Remuneration: Enter the periodical amount to the Employee Record

PAYSLIP PROCESSING WITH SHARE BASED REMUNERATION

From the above settings, the Share Based Remuneration benefit value will be included in each periodical payroll.

As explained earlier, the Employee PRSI subclass may differ to the Employer PRSI subclass as the amounts subject to employee and employer PRSI now differ.

Share Based Remuneration: Entering value to the employees payroll

The Benefit captured will be itemised on the employees payslip.

Share Based Remuneration: Employee payslip itemising the gain

The deductions made from the gain in this manner will flow through to the P30 for inclusion in the subsequent P30 return to be made to Revenue.

P35 REPORTING

For 2017, and all subsequent years, Revenue require the reporting of the benefit value of Share Based Remuneration on an employee by employee basis on the Year End Statement, as advised in the Revenue issued Advanced Notice.

The net value means the difference between the market value of the shares awarded and the amount paid by the employee for the shares, where this results in a discount price on the shares, it is this 'discount' which is deemed to give rise to a benefit to the employee.

Any gains arising from the disposal of the shares (proceeds less cost) is within the scope of Capital Gains Tax and is not relevant in the context of Share Based Remuneration. Revenue have issued a specific Tax Manual in relation to Share Based Remuneration.

MEANING OF SHARE BASED REMUNERATION

Share Based Remuneration has a specific meaning for PRSI purposes and is defined in section 2(1) of the Social Welfare Consolidation Act (as amended by Section 10 of the Social Welfare and Pensions Act 2012 and Section 4 of the Social Welfare and Pensions Act 2014). It essentially means remuneration given to an employee in the form of shares (including stock and securities) in the company in which the employee holds his or her office or employment, or in a company which has control of that company.

Shares in any other company do not come within the definition of Share Based Remuneration. All types of share option gains come within the definition.

SHARE AWARDS - THE CHARGE TO PRSI

Remuneration in the form of shares in companies other than that in which the employee holds his or her office or employment, or in a company which has control of that company, has been within the PAYE system since 2004 and remains fully chargeable to both employee and employer PRSI.

Remuneration in the form of shares in the company in which the employee holds his or her office or employment, or in a company which has control of that company, all such share-based remuneration is chargeable to employee PRSI. Employer PRSI is not chargeable.

AMOUNT CHARGEABLE TO PRSI

The receipt of shares by an employee is treated as a perquisite for income tax purposes and the rules that apply to the taxation of notional pay also apply for Employee PRSI purposes. Refer to Revenue guide to Benefit in Kind for further information on the related taxation rules and to what it applies.

RECORDING OF PRSI

As Share Based Remuneration is derived from insurable employment, it should be recorded under the PRSI Class applying to the employee at the time he or she receives the shares (if subject to vesting, the time of vesting) or exercises the share options, as the case may be, even if any benefit or gain accrues to the individual after he or she has left the particular employment.

Because the amount that is chargeable to PRSI is different for employees and employers it may attract different PRSI subclasses.

Where this occurs the return must always be made at the employee's subclass.

Example:

If a Class A employee has weekly pay of €350 and, in a particular week, has a derived benefit from the issue of shares of €450.

Employee PRSI is calculated on income of €800 - Subclass A1.

Employer PRSI is calculated on income of €350 - Subclass AO.

Employer and employee PRSI should be added together as normal.

Share Based Remuneration: Varying PRSI Subclasses between the employee and employer

PAYMENT OF PRSI

The obligation to deduct and remit PRSI in respect of Share Based Remuneration generally rests with the employer. Accordingly the PRSI payable should be deducted by the employer through payroll along with other PRSI liabilities and remitted to the Collector General with the monthly P30 return.

SHARE OPTION - GAINS

Shares purchased through a Share Option scheme are purchased from an employee's net take home pay. The benefit that the employee may get from exercising a share option is that the option price for buying the shares is less that the market value of the share. The difference between the option price and the market value represents a gain for the employee.

The taxation of gains on the exercise of share options comes within the special self-assessment regime. Income tax known as ‘relevant tax on share options’ (RTSO) is payable within 30 days of an option being exercised and is outside the PAYE collection system. Form RTSO1 must be completed and returned to the Collector General within 30 days of the date of exercise. USC and PRSI on such gains must also be included on the Form RTSO1and remitted, together with the income tax due, within 30 days of exercise.

Refer to the Revenue issued Form CG16 for further information.

SAVE AS YOU EARN SCHEMES (SAYE)

Gains made on the exercise of share options received under Revenue approved SAYE schemes are not chargeable to income tax. In the case of share options exercised when the individual is still employed by the company that granted the share option, the obligation to deduct and remit PRSI rests with that employer. Accordingly, the PRSI should be deducted by the employer through payroll along with other PRSI liabilities and remitted to the Collector General with the monthly P30.

Where a share option is exercised after the individual has left the employment, the obligation to pay the PRSI falls instead on that individual. PRSI should be paid directly to the Department of Social Protection's Special Collection Section within 30 days after the share option has been exercised. Form SBR1 is to be used for this purpose.

PAYMENT ARRANGEMENTS

Share Based Remuneration: Payment Arrangements

PROCESSING SHARE BASED REMUNERATION IN COLLSOFT

Once an employee and employer enter into a shares agreement, the employer must establish which if the categories the share falls into; Share Based Remuneration or a Share option. Once confirmed the employer will identify if it falls into the PAYE collection system and their obligations to deduct and remit the necessary PAYE, USC and PRSI derived from the resulting gains on exercise/vesting.

Recording share gains in CollSoft in order to make the necessary deduction the gains whould be treated as a Benefit in Kind.

To apply the correct treatment of PAYE, USC, and EmployEE PRSI (but not EmployER PRSI) CollSoft offers a specific Share Based Remuneration flag within Benefit settings.

The first step is to assign a Benefit in Kind setting to 'Share Based Remuneration' at Company level.

ASSIGN A BIK ELEMENT TO TREAT SHARE BASED REMUNERATION

- Select Company> Edit Company>

- Select the BIK (Benefit in Kind) tab from this Company screen

- Rename a BIK element to easily identify it's purpose, e.g. Share Based Remuneration, this will also display on the employees payslip

- Flag the dedicated Share Based Remuneration flag against the Benefit item you have assigned for this purpose.

Share Based Remuneration: Assign a BIK element at Company level

UPDATE THE EMPLOYEE RECORD WITH THE PERIODICAL VALUE

Now that there is a dedicated BIK element, the notional value of the associated share remuneration should be captured within the employees periodical payroll to which it relates (the approriate date to make the deductions should be decided on based on the circumstance in compliance with the Revenue rules for remittance).

- Select the Employee record

- Select the BIK tab

- The previously assigned BIK element will be displayed by the name allocated at Company level

- Enter the periodical value as appropriate to the pay frequency

- The 'Total Share Based Remuneration' field will automate the year to date total as each wage period is processed.

Share Based Remuneration: Enter the periodical amount to the Employee Record

PAYSLIP PROCESSING WITH SHARE BASED REMUNERATION

From the above settings, the Share Based Remuneration benefit value will be included in each periodical payroll.

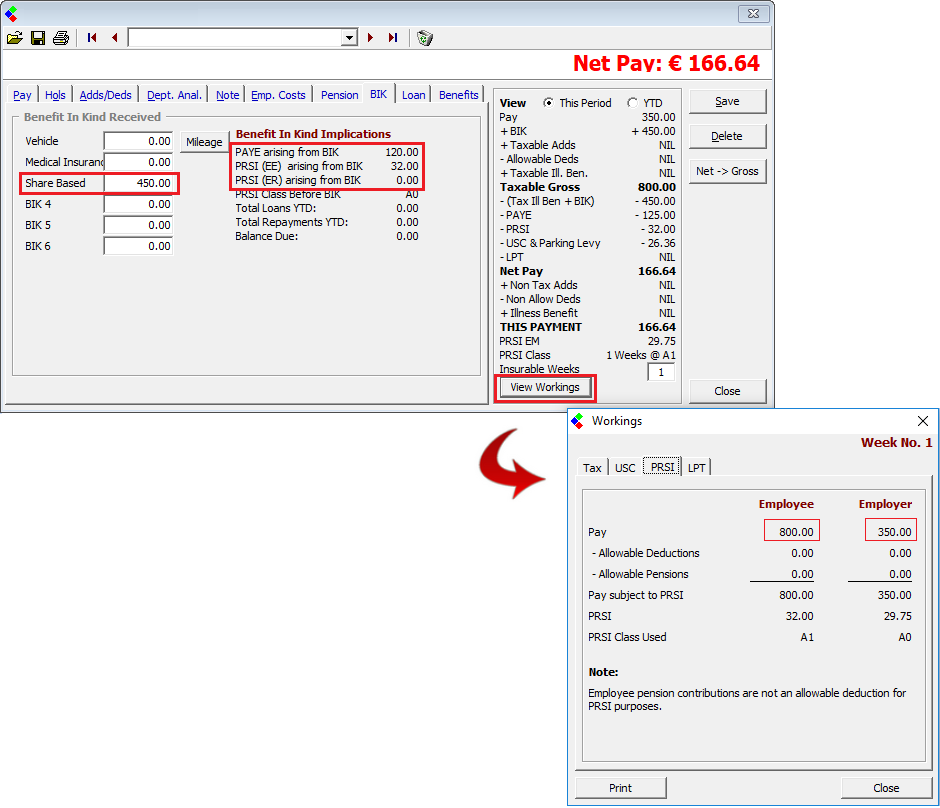

- Select the Employees periodical payslip

- Select the BIK tab

- The previously assigned BIK element will be displayed by the name allocated at Company level

- The periodical value added to the Employee record will display.

- A summary of the Benefit PAYE and PRSI implications will be calculated on screen

- The calculation of the PRSI can be further viewed by choosing to 'View Workings'

As explained earlier, the Employee PRSI subclass may differ to the Employer PRSI subclass as the amounts subject to employee and employer PRSI now differ.

Share Based Remuneration: Entering value to the employees payroll

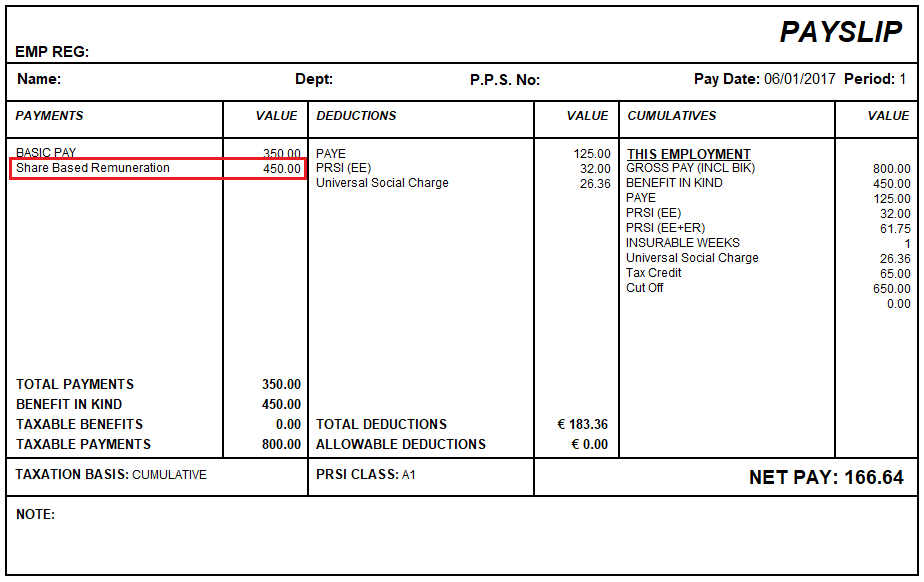

The Benefit captured will be itemised on the employees payslip.

Share Based Remuneration: Employee payslip itemising the gain

The deductions made from the gain in this manner will flow through to the P30 for inclusion in the subsequent P30 return to be made to Revenue.

P35 REPORTING

For 2017, and all subsequent years, Revenue require the reporting of the benefit value of Share Based Remuneration on an employee by employee basis on the Year End Statement, as advised in the Revenue issued Advanced Notice.

Assign BIK at Company Level.png

Assign BIK at Company Level.png

Final Payslips.png

Final Payslips.png

Payslip Working.png

Payslip Working.png

Setting up periodical amount.png

Setting up periodical amount.png

Share Based Remuneration - Actions.png

Share Based Remuneration - Actions.png

Share-Based Remuneration - Varying PRSI Classes.png

Share-Based Remuneration - Varying PRSI Classes.png

Get help for this page

Get help for this page