The Revenue Temporary COVID-19 Wage Subsidy Scheme

Posted 16:15 25th March 2020

The new Temporary COVID-19 Wage Subsidy Scheme is far more complicated than the previous Employer COVID-19 Refund Scheme and this guide is intended as an overview of the new scheme.

We would ask our customers to understand that CollSoft does not develop software based on reports from RTE News, the Irish Independent or some rambling tweets on Twitter - we develop our software based on the facts as published by Revenue. It may well be the case that some news outlet has a scoop on what is happening next, but if Revenue don't confirm we wont develop it.

The details of this new scheme announced on 24th March 2020 can be found on the Revenue website at

https://www.revenue.ie/en/corporate/communications/covid19/temporary-covid-19-wage-subsidy-scheme.aspx

We would also ask customers to remember that even when Revenue publish details, it takes us time to develop, test, document and deploy software updates. Often times we will make decisions about particular developments that are rooted in common sense and designed to protect our customers from future problems. One example of this was the decision to not allow users to process COVID 19 refunds in monthly payrolls for March. This would have triggered an automatic refund from Revenue of €812 which was impossible for you to have paid to your employees. We advised customers to switch over to a weekly pay frequency for very good reasons.

If Revenue published something yesterday, don't email us today asking why the update is not available and tell us that "if you fail to provide an appropriate solution here, we will be opting for an alternative provider next year." and "I very much hope that you can offer us the service and professionalism that your customers deserve." (extracts from an actual email from a customer this week)

Honestly, if anybody feels that we are lacking in our response to this COVID-19 crisis then please let me know and I will personally arrange for a full refund of any licence fees and send you the contact details for Sage, Thesaurus, Brightpay, Big Red Book or any other providers and you can see how responsive they are to the evolving situation. Please, let common sense apply.

We will be publishing an initial update on Thursday afternoon to enable employers to file under the new scheme. This first update will be functional, but very basic in its operation.

Over the next few days we will release subsequent updates which will make the process easier, but I hope that when you read the guidelines below you will understand that it takes some time to develop comprehensive solutions.

The aim is that by Thursday afternoon users will be able to start making filings under the new system and over the weekend we will follow up with more updates that makes the process easier to follow.

I would like to thank all of our customers for bearing with us during this difficult time.

Thanks,

Jason Collins

Managing Director

CollSoft Limited

And now, onto the main feature...….

Background To the New Scheme

The Government yesterday announced that the current "Employer COVID-19 Refund Scheme" was being replaced by a new scheme called the "Temporary COVID-19 Wage Subsidy Scheme" from Thursday 26th March.

The existing "Employer COVID-19 Refund Scheme" was an emergency scheme from the Department of Employment Affairs and Social Protection (but administered by Revenue) where Employers were able to make an emergency payment of €203 per week to employees who would otherwise have been laid off.

The new "Temporary COVID-19 Wage Subsidy Scheme" is a completely different scheme from Revenue to directly subsidise an employee's salary.

Please Note:

There has been some confusion among employers regarding the €203 payment available under the "Employer COVID-19 Refund Scheme". This payment has not been increased to €350. The only employees who will recieve the increased payment of €350 are those who have actually ceased employment and are in receipt of Jobseekers benefit directly from the Department of Employment Affairs and Social Protection.

Employers are NOT allowed to make tax free payments of €350 to employees who have been temporally laid off (but not actually ceased)

The new "Temporary COVID-19 Wage Subsidy Scheme"

Under the new scheme Employers will be able to make a tax free payment to employees that is equivalent to 70% of their average "After Tax" pay for which they will receive a direct subsidy from Revenue. This subsidy is capped at a maximum of either €350 or €410 depending on what the average "After Tax" pay. As this average goes up, the available subsidy goes down.

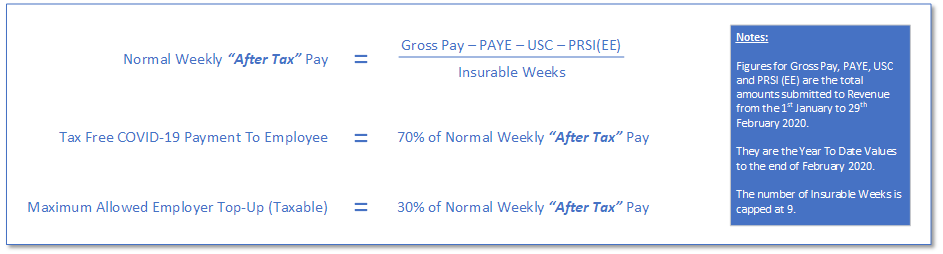

"After Tax" Pay is defined as Gross Pay - PAYE - USC - PRSI (EE). The average value for this "After Tax" Pay is based on the submissions made to Revenue for the employee between 1st January and 29th February 2020

In addition to this, employers will be able to make an additional "Top-Up" payment of up to 30% of the "After Tax" Pay, however this top-up amount is subject to PAYE and USC and PRSI at "J9" rates.

Employers who top up by more than 30% will have their subsidy reduced on a like for like basis, so for every Euro above the 30% amount the employer will receive a Euro less from Revenue by way of a subsidy.

The following outlines the calculations involved;

How is it being implemented by Revenue?

This scheme is going to be implemented in two distinct phases

Phase I - 26th March to 20th April

Employers will be required to calculate what each employee's average "After Tax" pay is based on the submissions made to Revenue in the period from 1st January to 29th February 2020.

The employer then calculates the "Tax Free COVID-19 Payment" as 70% of the average "After Tax" Pay.

This "Tax free COVID-19 Payment" is limited depending on the average "After Tax" Pay as outlined below;

Having established the value of the "Tax free COVID-19" payment, the employer is now ready to decide if they are going to make a "Top-Up" payment.

As outlined earlier this top up is subject to PAYE, USC and PRSI at class J9.

"Top-Up" higher than 30% of the average "After Tax" pay will reduce the amount of subsidy that Revenue will pay on a Euro for Euro Basis. If you breach the 30% limit by €50 then Revenue will reduce your subsidy by €50.

In Phase I Revenue will automatically pay a subsidy of €410 per week for every J9 submission received, even if the amount of the "Tax Free COVID-19 Payment" is less than that.

The important point to note here is that Revenue always refund €410, even though you may have actually paid the employee less than that under the scheme.

The Employer will be required to account for this over payment, and they will be required to refund it back to Revenue at a later date.

Phase II - After 20th April

In Phase II Revenue will have introduced a new PMOD Payroll Submission process that will enable employers to report the exact amount paid to the employees under the scheme.

Revenue will then issue the subsidy payments based on these new employer submissions, and the amounts paid by Revenue will match the amounts paid to employees.

What Happens after that?

At this stage all I can say is that Revenue plan to reconcile all subsidies down to the last Euro, and employers will be required to account for all subsidies claimed under the scheme.

In Phase I Revenue will pay a subsidy of €410 regardless of what you pay your employees. Where you have paid less to your employees Revenue will want their money back.

You will need to account for this.

Phase II will see more control over the mount of subsidies paid, but it is still possible that some employees who have more than one employment may receive payments higher than what they are entitled to receive. In these cases Revenue are likely to claw this back from employees via their end of year statements.

This is a complicated scheme which has been developed in a very short space of time. It is not perfect, but it is aimed at enabling employers and employees to make it through this current crisis.

Employers will find Revenue to be relatively sympathetic in cases where they have made honest mistakes in how they have operated the scheme. However, any employer who tries to take advantage of the scheme will be asked to account for their actions and can not expect any sympathy from Revenue or the Irish tax payer.

The new Temporary COVID-19 Wage Subsidy Scheme is far more complicated than the previous Employer COVID-19 Refund Scheme and this guide is intended as an overview of the new scheme.

We would ask our customers to understand that CollSoft does not develop software based on reports from RTE News, the Irish Independent or some rambling tweets on Twitter - we develop our software based on the facts as published by Revenue. It may well be the case that some news outlet has a scoop on what is happening next, but if Revenue don't confirm we wont develop it.

The details of this new scheme announced on 24th March 2020 can be found on the Revenue website at

https://www.revenue.ie/en/corporate/communications/covid19/temporary-covid-19-wage-subsidy-scheme.aspx

We would also ask customers to remember that even when Revenue publish details, it takes us time to develop, test, document and deploy software updates. Often times we will make decisions about particular developments that are rooted in common sense and designed to protect our customers from future problems. One example of this was the decision to not allow users to process COVID 19 refunds in monthly payrolls for March. This would have triggered an automatic refund from Revenue of €812 which was impossible for you to have paid to your employees. We advised customers to switch over to a weekly pay frequency for very good reasons.

If Revenue published something yesterday, don't email us today asking why the update is not available and tell us that "if you fail to provide an appropriate solution here, we will be opting for an alternative provider next year." and "I very much hope that you can offer us the service and professionalism that your customers deserve." (extracts from an actual email from a customer this week)

Honestly, if anybody feels that we are lacking in our response to this COVID-19 crisis then please let me know and I will personally arrange for a full refund of any licence fees and send you the contact details for Sage, Thesaurus, Brightpay, Big Red Book or any other providers and you can see how responsive they are to the evolving situation. Please, let common sense apply.

We will be publishing an initial update on Thursday afternoon to enable employers to file under the new scheme. This first update will be functional, but very basic in its operation.

Over the next few days we will release subsequent updates which will make the process easier, but I hope that when you read the guidelines below you will understand that it takes some time to develop comprehensive solutions.

The aim is that by Thursday afternoon users will be able to start making filings under the new system and over the weekend we will follow up with more updates that makes the process easier to follow.

I would like to thank all of our customers for bearing with us during this difficult time.

Thanks,

Jason Collins

Managing Director

CollSoft Limited

And now, onto the main feature...….

Background To the New Scheme

The Government yesterday announced that the current "Employer COVID-19 Refund Scheme" was being replaced by a new scheme called the "Temporary COVID-19 Wage Subsidy Scheme" from Thursday 26th March.

The existing "Employer COVID-19 Refund Scheme" was an emergency scheme from the Department of Employment Affairs and Social Protection (but administered by Revenue) where Employers were able to make an emergency payment of €203 per week to employees who would otherwise have been laid off.

The new "Temporary COVID-19 Wage Subsidy Scheme" is a completely different scheme from Revenue to directly subsidise an employee's salary.

Please Note:

There has been some confusion among employers regarding the €203 payment available under the "Employer COVID-19 Refund Scheme". This payment has not been increased to €350. The only employees who will recieve the increased payment of €350 are those who have actually ceased employment and are in receipt of Jobseekers benefit directly from the Department of Employment Affairs and Social Protection.

Employers are NOT allowed to make tax free payments of €350 to employees who have been temporally laid off (but not actually ceased)

The new "Temporary COVID-19 Wage Subsidy Scheme"

Under the new scheme Employers will be able to make a tax free payment to employees that is equivalent to 70% of their average "After Tax" pay for which they will receive a direct subsidy from Revenue. This subsidy is capped at a maximum of either €350 or €410 depending on what the average "After Tax" pay. As this average goes up, the available subsidy goes down.

"After Tax" Pay is defined as Gross Pay - PAYE - USC - PRSI (EE). The average value for this "After Tax" Pay is based on the submissions made to Revenue for the employee between 1st January and 29th February 2020

In addition to this, employers will be able to make an additional "Top-Up" payment of up to 30% of the "After Tax" Pay, however this top-up amount is subject to PAYE and USC and PRSI at "J9" rates.

Employers who top up by more than 30% will have their subsidy reduced on a like for like basis, so for every Euro above the 30% amount the employer will receive a Euro less from Revenue by way of a subsidy.

The following outlines the calculations involved;

How is it being implemented by Revenue?

This scheme is going to be implemented in two distinct phases

Phase I - 26th March to 20th April

Employers will be required to calculate what each employee's average "After Tax" pay is based on the submissions made to Revenue in the period from 1st January to 29th February 2020.

The employer then calculates the "Tax Free COVID-19 Payment" as 70% of the average "After Tax" Pay.

This "Tax free COVID-19 Payment" is limited depending on the average "After Tax" Pay as outlined below;

- Average Pay from €0 to €586 limits it to €410

- Average Pay from €586 to €960 limits it to €350

- Average Pay above €960 is not entitled to the subsidy

Having established the value of the "Tax free COVID-19" payment, the employer is now ready to decide if they are going to make a "Top-Up" payment.

As outlined earlier this top up is subject to PAYE, USC and PRSI at class J9.

"Top-Up" higher than 30% of the average "After Tax" pay will reduce the amount of subsidy that Revenue will pay on a Euro for Euro Basis. If you breach the 30% limit by €50 then Revenue will reduce your subsidy by €50.

In Phase I Revenue will automatically pay a subsidy of €410 per week for every J9 submission received, even if the amount of the "Tax Free COVID-19 Payment" is less than that.

The important point to note here is that Revenue always refund €410, even though you may have actually paid the employee less than that under the scheme.

The Employer will be required to account for this over payment, and they will be required to refund it back to Revenue at a later date.

Phase II - After 20th April

In Phase II Revenue will have introduced a new PMOD Payroll Submission process that will enable employers to report the exact amount paid to the employees under the scheme.

Revenue will then issue the subsidy payments based on these new employer submissions, and the amounts paid by Revenue will match the amounts paid to employees.

What Happens after that?

At this stage all I can say is that Revenue plan to reconcile all subsidies down to the last Euro, and employers will be required to account for all subsidies claimed under the scheme.

In Phase I Revenue will pay a subsidy of €410 regardless of what you pay your employees. Where you have paid less to your employees Revenue will want their money back.

You will need to account for this.

Phase II will see more control over the mount of subsidies paid, but it is still possible that some employees who have more than one employment may receive payments higher than what they are entitled to receive. In these cases Revenue are likely to claw this back from employees via their end of year statements.

This is a complicated scheme which has been developed in a very short space of time. It is not perfect, but it is aimed at enabling employers and employees to make it through this current crisis.

Employers will find Revenue to be relatively sympathetic in cases where they have made honest mistakes in how they have operated the scheme. However, any employer who tries to take advantage of the scheme will be asked to account for their actions and can not expect any sympathy from Revenue or the Irish tax payer.

| Files | ||

|---|---|---|

| Temporary COVID-19 Wage Subsidy Scheme.png | ||

Get help for this page

Get help for this page