Directors Fees

WHAT ARE DIRECTORS FEES

Directorship fees paid by Irish incorporated companies are always chargeable to Irish tax under Schedule E and should be subject to appropriate PAYE, PRSI and USC.

Director's fees are defined as fees relating solely to attending board meetings and other specific directors duties and not remuneration under a contract of service. Any such fees paid to a Director in respect of duties as an officer of the company are generally insurable under Class S – this means there is no obligation on the employer to play employer PRSI.

However, it should be noted that Executive directors, who do not specifically receive director’s fees and who are paid by the company for duties as both an officer and those as an employee under a contract of employment, are generally subject to Class A PRSI, which result in an employer PRSI cost of 10.75%.

PRSI AND DIRECTORS FEES

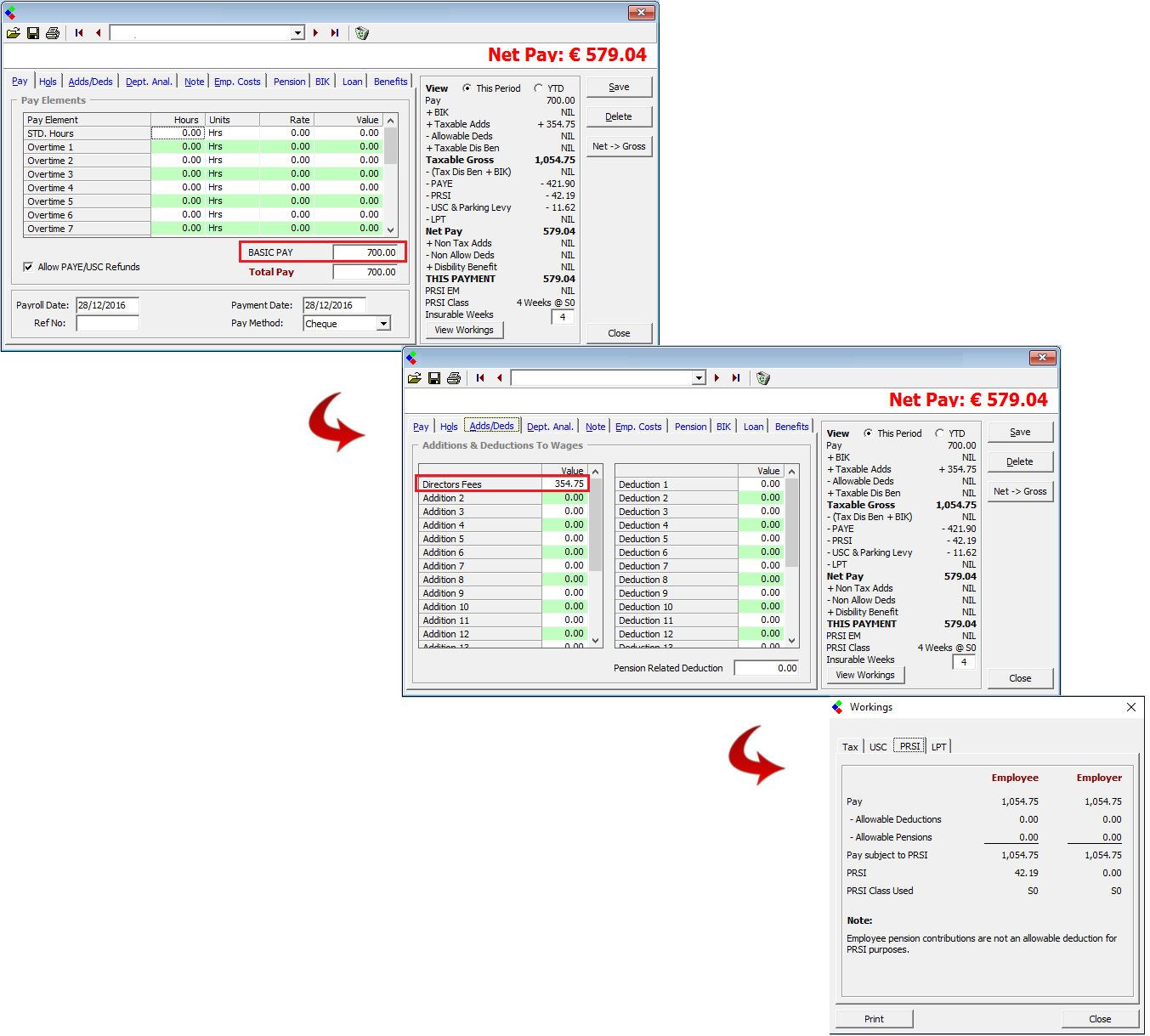

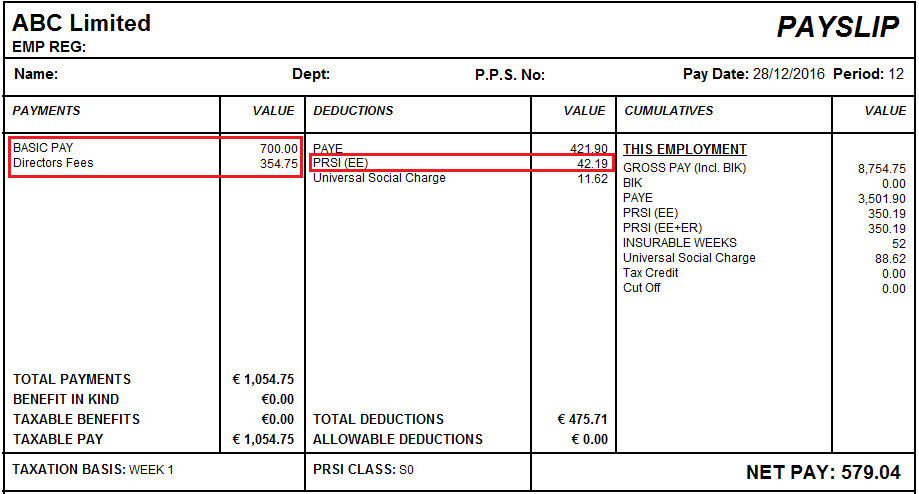

Directors Fees, as defined above, are subject to PRSI at a flat rate of 4% therefore, any payment of such fees should be classified as reckonable pay within the payroll.

For 2016, Class S applies a flat 4% to total pay, i.e. there is no PRSI allowance, therefore the entire income (remuneration and fees) can be entered as pay for Tax and PRSI purposes. The correct PRSI deduction of 4% will be applied to the Directors Fee portion of the payment.

For clarity to the compilation of payments to Directors, the payment of Directors Fees should be itemised from normal remuneration by setting up a specific Taxable Addition within the wages record of the Director, even if there is no periodical remuneration within the particular pay period.

It is advisable to confirm the treatment of payments to Directors with your accountant/tax advisor if you are in any doubt to whether or not any portion of income is to be treated as Directors Fees.

Directorship fees paid by Irish incorporated companies are always chargeable to Irish tax under Schedule E and should be subject to appropriate PAYE, PRSI and USC.

Director's fees are defined as fees relating solely to attending board meetings and other specific directors duties and not remuneration under a contract of service. Any such fees paid to a Director in respect of duties as an officer of the company are generally insurable under Class S – this means there is no obligation on the employer to play employer PRSI.

However, it should be noted that Executive directors, who do not specifically receive director’s fees and who are paid by the company for duties as both an officer and those as an employee under a contract of employment, are generally subject to Class A PRSI, which result in an employer PRSI cost of 10.75%.

PRSI AND DIRECTORS FEES

Directors Fees, as defined above, are subject to PRSI at a flat rate of 4% therefore, any payment of such fees should be classified as reckonable pay within the payroll.

For 2016, Class S applies a flat 4% to total pay, i.e. there is no PRSI allowance, therefore the entire income (remuneration and fees) can be entered as pay for Tax and PRSI purposes. The correct PRSI deduction of 4% will be applied to the Directors Fee portion of the payment.

For clarity to the compilation of payments to Directors, the payment of Directors Fees should be itemised from normal remuneration by setting up a specific Taxable Addition within the wages record of the Director, even if there is no periodical remuneration within the particular pay period.

It is advisable to confirm the treatment of payments to Directors with your accountant/tax advisor if you are in any doubt to whether or not any portion of income is to be treated as Directors Fees.

Directors Fees - Payslip.png

Directors Fees - Payslip.png

Directors Fees - Setting it up in the Payroll.png

Directors Fees - Setting it up in the Payroll.png

| Files | ||

|---|---|---|

| Directors Fees - Payslip.png | ||

| Directors Fees - Setting it up in the Payroll.png | ||

Get help for this page

Get help for this page